How can the war with Iran affect oil and gas markets?

- Mar 3

- 3 min read

Updated: Mar 6

The Strait of Hormuz, located between Iran and the United Arab Emirates, is one of the most critical arteries of global trade. Around 30 percent of the world’s oil supply and about 20 percent of seaborne liquefied natural gas pass through it. At its narrowest point, the strait is just 33 kilometers wide, with shipping lanes only about 3 kilometers wide in each direction.

Because of its location, it serves as a crucial chokepoint for oil deliveries from OPEC countries to customers in Asia and beyond.

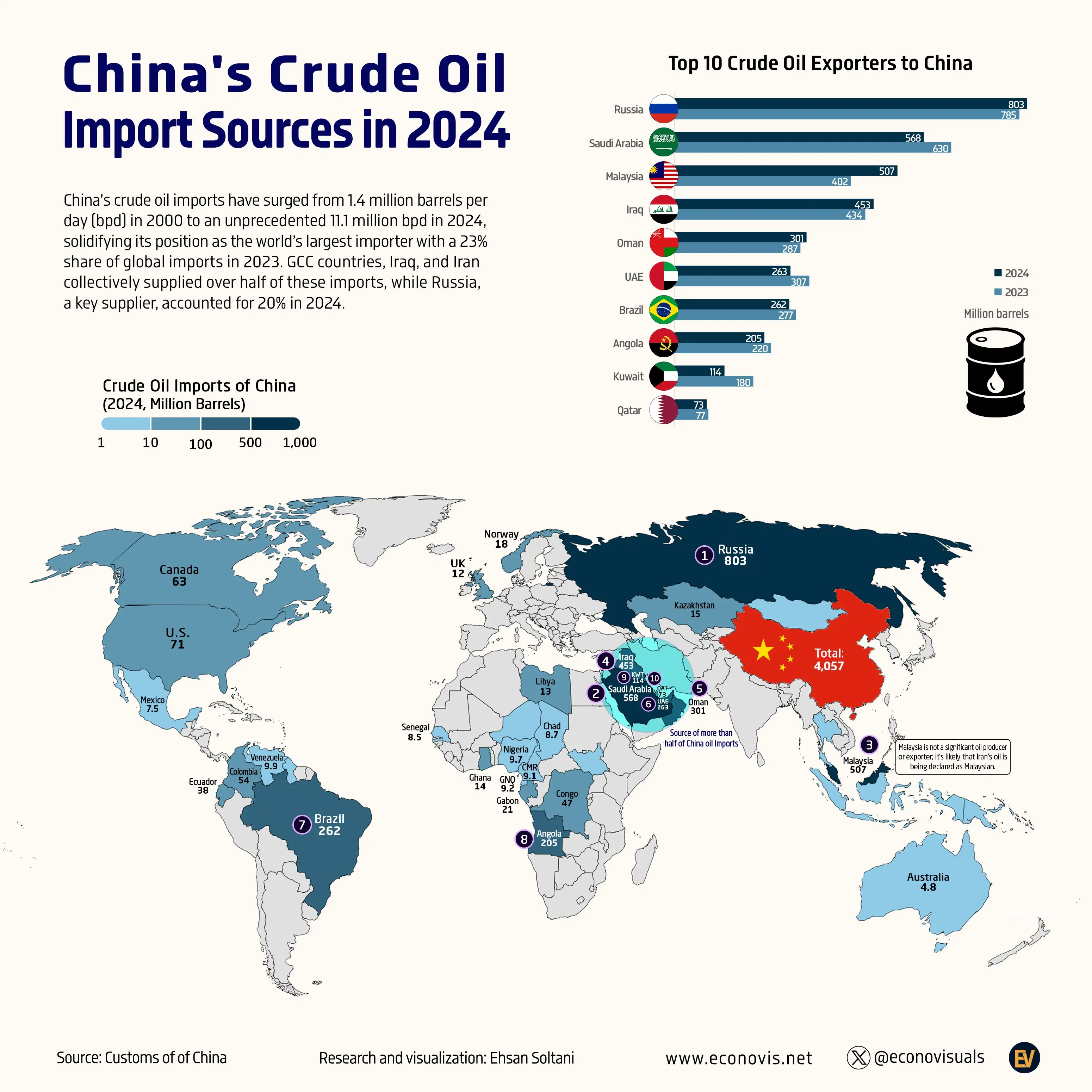

A few hours ago, Iran announced that it intends to shut down the Strait of Hormuz and warned that any vessel attempting to approach it would be destroyed. This move could hurt Iran more in the medium term than its enemies, as China buys around 90% of the oil that Iran exports, which is internationally sanctioned.

Although Iran’s crude exports account for only about 3 to 4 percent of the global market, it's importance extends well beyond its own production. The country’s geopolitical weight is rooted in its strategic position, its influence over regional security dynamics, and its capacity to disrupt critical energy infrastructure and transit routes.

Additionally, Iran holds the world’s fourth-largest proven oil reserves, representing about 9 percent of global crude supplies. Only Venezuela, Saudi Arabia, and Canada possess larger reserves.

Decades of political unrest, economic mismanagement, war, and sanctions reduced Iran’s crude production from a peak of approximately 6 million barrels per day in 1974 to around 3.5 million barrels per day. However, in the previous months before the current war, output had climbed to historic highs despite US sanctions, largely because of Iran’s close ties with China.

Asian countries are the most affected by the current disruption of the Hormuz oil trade:

Last year, more than 80 percent of the crude oil and LNG passing through the strait was destined for Asian markets. Because Japan and South Korea get around 90% of their oil imports from the Strait, it is likely that their supplies will increasingly come from the US but at higher prices.

With the war, oil prices have increased around 20% in international markets. When Qatar suspended LNG supplies, European gas prices surged by 45 percent in the last week, highlighting how disruptions in the region quickly reverberate worldwide.

Saudi Arabia and the United Arab Emirates have developed alternative pipeline routes that bypass the Hormuz Srait and export their oil and gas. Together, these pipelines can transport an additional 2.6 million barrels per day to global markets, equivalent to roughly 40 percent of their normal crude exports. While this provides an important mitigating factor, it does not fully offset the risks associated with a prolonged closure.

So far, Tehran has not targeted the Saudi and Emirati pipelines designed to circumvent Hormuz. If it were to do so, oil prices would likely rise further. However, current supply buffers could limit the risk of severe market dislocation. Saudi Arabia and Qatar have also announced the will stop their operations at several major oil and gas facilities following Iranian missile and drone attacks, adding another layer of uncertainty to global energy supplies.

A sustained blockade of the Strait of Hormuz could significantly damage China’s economy, as around 50% of its oil purchases are delivered through that passage. Same with Indian economy, which imports about 50% of its oil through the strait. This would likely increase purchases from Russia, which could be benefited from oil price increases, but would lose drones deliveries from its close ally Iran.

The United States, by contrast, is no longer heavily dependent on Middle Eastern oil. As a net energy producer, higher global prices could benefit US oil companies. It may take several weeks before rising global prices translate into substantially higher fuel costs for American consumers, but the political and economic impact would eventually be felt.

Comments